Episodes of rupee depreciation against the US dollar routinely trigger heightened concern within India’s public discourse. Currency movement is often interpreted as a proxy for economic distress, prompting disproportionate alarm across media and commentary.

This interpretation, however, overlooks the more analytically relevant question: why does India’s economy continue to expand strongly even as the rupee adjusts downward? The answer lies not in episodic market fluctuations, but in structural shifts that have decoupled growth dynamics from nominal exchange rate movements.

As the Indian Rupee navigated record lows against the USD through late 2024 and 2025, breaching the psychologically loaded 90 mark, India’s GDP was not slowing down. It was accelerating. Growth peaked at 8.2% in Q2 of FY 2025-26, making India the fastest-growing major economy in the world at precisely the moment when its currency was supposedly “weakening”.

The RBI Is Not Defending Ego, It Is Managing Reality.

The Reserve Bank of India is often misunderstood. It is not trying to “save” the rupee. It is trying to prevent disorder.

India does not run a fixed exchange rate. It runs a managed float. The difference matters. The RBI does not fight the market’s direction. It manages the pace.

Between September and November 2024, as global dollar strength intensified, the RBI intervened decisively but strategically. In November 2024 alone, it conducted a net spot market sale of $20.23 billion, the highest monthly intervention since 2008. At the same time, it leaned heavily on the forward market, with net short forward positions expanding from $14.6 billion in September to $49.2 billion in October, and nearly $60 billion by end-November.

Even after this intense intervention cycle, India’s foreign exchange reserves remained resilient. Reserves stood at $705 billion in September 2024, dipped during peak defence, and then recovered to $697.9 billion by June 2025, settling at $688.1 billion by September 2025, even after cumulative spot sales of nearly $50 billion.

The RBI is deliberately using forwards as a bridge, managing volatility without permanently burning reserves. It smoothens the glide path so that the real economy gets time to adjust.

Why the IMF Changed Its Language on India

This shift has not gone unnoticed globally. The IMF reclassified India’s exchange rate regime from “stabilised” to a “crawl-like arrangement,” acknowledging that while the rupee moves, it now does so along a controlled and observable path.

This matters because it reflects a deeper policy maturity. The RBI is allowing more two-way movement than before. Realised currency volatility crossed 5% in 2025, compared to a historical average of below 2%. That flexibility helps absorb external shocks more efficiently and reduces the need for endlessly accumulating reserves at high cost.

In simple terms, policy now treats exchange rate volatility as a variable to be managed rather than eliminated.

Liquidity Support Without Losing Control

Currency management does not operate in isolation. Every forex intervention affects domestic liquidity, and the RBI has responded well.

In December 2025, the RBI announced a two-pronged liquidity injection exceeding ₹1.6 lakh crore. This included two OMO (Open Market Operations) purchase tranches of ₹50,000 crore each on December 11 and 18, along with a $5 billion USD/INR Buy-Sell Swap on December 16, injecting roughly ₹61,500 crore into the system.

The objective was not short-term stimulus, but durable liquidity, ensuring that past rate cuts are transmitted into credit growth without destabilising inflation or the exchange rate.

Growth and Currency Are No Longer Tied at the Hip

The biggest mistake in the rupee debate is assuming that currency strength and economic strength must move together.

The rupee reacts to global interest rates, capital flows, oil prices, and dollar dominance. India’s GDP growth today is anchored in domestic consumption, public capex, services exports, manufacturing depth, and digital formalisation.

Fast growth actually raises imports. A growing economy imports more machinery, electronics, and energy. That widens the trade deficit in the short term and puts pressure on the currency. Ironically, rapid growth can weaken the rupee even as it strengthens the country.

The Rupee Is Not Weak. It Is Competitive.

In real terms, several measures suggested the rupee was persistently overvalued. Adjusted for inflation and trade weights, the Real Effective Exchange Rate (REER) showed signs of correction in 2024-25.

That correction improves export competitiveness and cushions the current account. Services exports, IT, pharmaceuticals, agriculture, and especially Global Capability Centres benefit directly.

Every dollar earned by a GCC is almost pure forex retention. No heavy import leakage. This is why services exports now quietly act as India’s external stabiliser.

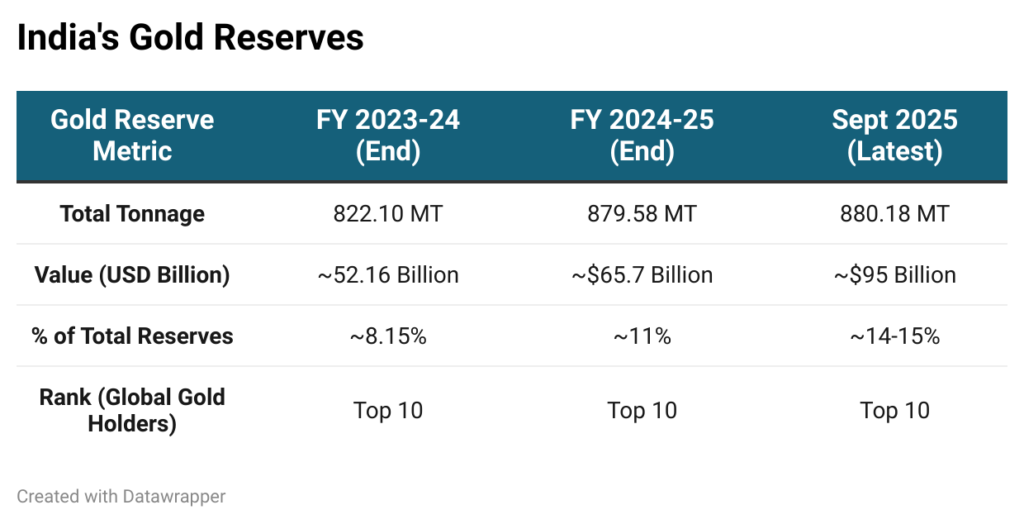

Gold: The Quiet Signal of Confidence

One of the least discussed shifts is the RBI’s gold strategy.

India’s gold reserves have steadily expanded from 822.10 metric tonnes in FY24 to 879.58 MT in FY25, reaching 880.18 MT by September 2025. Gold now accounts for 14-15% of total reserves, up from 8.15% just two years earlier.

In value terms, gold holdings rose from roughly $65.7 billion to nearly $95 billion, aided both by accumulation and a sharp rise in global gold prices. India remains among the top ten gold-holding central banks globally.

Gold is not tactical. It is strategic. It diversifies risk, hedges inflation, and signals long-term balance sheet strength.

The RBI Is Not Losing Money. It Is Making It.

Currency management has also delivered a fiscal dividend.

In FY 2024-25, the RBI transferred a record surplus of ₹2.69 trillion to the central government, a 27.37% increase year-on-year. This came alongside an 8.2% expansion of the RBI’s balance sheet to ₹76.25 lakh crore, with income rising 22.77% while expenditure grew just 7.76%.

Gold holdings surged 52.09%, and even the digital rupee saw a 334% expansion, reflecting institutional experimentation without fiscal recklessness.

Risks Exist. But They Are Contained.

Yes, prolonged intervention reduces incentives for private hedging. By late 2024, unhedged external commercial borrowings stood at $65.49 billion, about 34.4% of ECBs (External Commercial Borrowings). That is a risk.

But markets adapt. By late 2025, firms began increasing hedge cover as expectations of prolonged rupee pressure settled in. Moral hazard exists, but it is neither ignored nor systemic.

The rupee is adjusting to a world of tight monetary conditions, geopolitical turbulence, and dollar dominance. India, meanwhile, is adjusting upward in manufacturing depth, service sophistication, digital efficiency, and domestic resilience. These two movements do not cancel each other out. They coexist.

A falling rupee is not a verdict on India’s economy. It is a reflection of global liquidity cycles. India’s growth, on the other hand, is increasingly generated from within.

This helps explain the RBI’s calm response, the continuation of growth, and why a weaker rupee has not translated into broader economic stress.

Author: Diksha Bohra, Public Policy Consultant